The Vein-to-Vein Problem: Can APAC's Cold Chain Carry Advanced Therapies?

06 July 2026 | Monday | Analysis

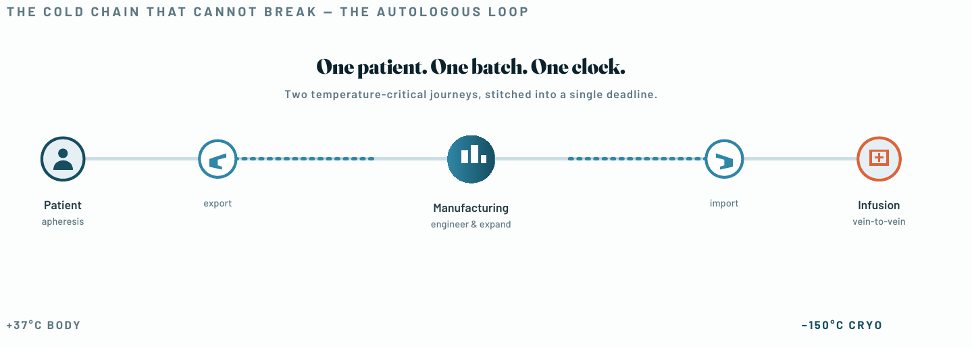

The requirement: a chain that cannot break

Key figures

- −150°C or colder — the temperature floor for most cell and gene therapies; some materials sit at −196°C in liquid nitrogen.

- 27 days — the median real-world vein-to-vein time for a leading CAR-T; shorter times track better response and survival.

- 1–18% — the reported manufacturing failure range — and for a batch of one, there is no second copy of the product.

- 12–96 hours — the shelf-life of fresh, un-frozen cells before they degrade — the reason freezing exists at all.

Somewhere over the South China Sea, inside a stainless-steel canister the size of a beer keg, a single patient’s living T-cells are riding at minus 150 degrees Celsius. They have been collected, flown to a manufacturing suite, engineered to hunt cancer, frozen again, and are now flying back. A telemetry tag pings the shipment’s temperature and coordinates every few minutes. The clock that matters is not measured in flight time. It is measured in the tolerance of frozen human cells for delay, mishandling, and the small catastrophes of a warm afternoon on a loading apron.

This is the defining paradox of advanced therapies in the Asia-Pacific. The science has largely been settled. CAR T-cell therapies have moved from experimental to standard of care for several blood cancers, and regulators across the region’s wealthiest markets have approved them. What has not been settled is whether the region can physically deliver them — reliably, repeatedly, and beyond a handful of elite metropolitan hospitals. Increasingly, the people who build these supply chains suspect that logistics, not biology, will decide who receives an advanced therapy and who is quietly ruled out.

To understand why, start with what an autologous therapy demands. Unlike a biologic manufactured in bulk, it is a batch of one. The patient’s own T-cells are extracted through leukapheresis, shipped to a facility, reprogrammed to recognise a tumour antigen, expanded, cryopreserved, and returned to the same patient. There are, in effect, two time- and temperature-critical supply chains stitched together: one from patient to factory, the other from factory back to patient. A break in either can end the treatment.

The temperature requirement is unforgiving. Most products must be held at minus 150 degrees or colder, achieved with liquid nitrogen in vapour-phase containers; some sit as low as minus 196. This is a different physical regime from ordinary pharmaceutical cold chain, where two-to-eight-degree refrigeration is the norm. At cryogenic temperatures, conventional refrigeration simply does not apply.

Then there is chain-of-identity, the requirement that quietly terrifies everyone in the process. Because the product is a single patient’s cells, it is not fungible. A vial cannot be swapped or reissued from stock. Every bag, label, freezer slot and infusion must be traceable to one named individual through an auditable, unbroken record. A mislabelled shipment is not an inventory error; it is a potential fatality. This is why cell-therapy logistics is described less as shipping and more as custody — a clinical responsibility that travels with the box.

“People imagine our job is moving a box from A to B. What we are actually protecting is a deadline written into the patient’s biology. The box is easy. The deadline is the product.”

— Cell-therapy supply-chain lead, multinational developer (APAC)

Finally, the whole system is judged by one metric: vein-to-vein time, the interval from leukapheresis to infusion. In one of the largest real-world analyses of a commercial CAR-T, drawn from a US registry across dozens of authorised centres, the median vein-to-vein time was 27 days — and shorter times were associated with meaningfully better complete-response rates and survival. For some myeloma therapies, real-world intervals have run past two months. Every day inside that window is a day a patient with aggressive, relapsed disease may deteriorate past the point of eligibility. Logistics is not a back-office function. It is a clinical variable that shows up in the outcomes data.

The APAC gap: distance, friction and the Tier-2 wall

If the requirement is a chain that cannot break, the Asia-Pacific presents a landscape almost purpose-built to break it. The region spans from Japan and Korea in the temperate north to Australia in the south, taking in the archipelagic sprawl of Indonesia and the Philippines, the mainland reach of India, and the dense clusters of Singapore, Taiwan and Hong Kong. There is no equivalent of a single regulatory bloc or a continuously connected interior. Advanced-therapy shipments move by air, across borders, through customs regimes never designed with living cells in mind.

A dry-vapour shipper holds cryogenic temperature for a validated window of roughly seven to fourteen days when handled correctly and kept upright. A delay at a single customs desk, a shipment left tilted on a tarmac, or a missed connection can quietly consume that budget before anyone notices. Liquid nitrogen and dry ice are both classified as hazardous for air transport, and the rules vary sharply by country. Dry ice, cheaper and easier than nitrogen, only holds around minus eighty degrees and sublimates fast; a misloaded dry-ice shipper can warm within a day to three days. More consequentially, a large share of countries restrict or prohibit dry-ice shipments outright, and several developing markets ban dry-ice imports altogether — complicating precisely the cross-border, multi-leg routing that APAC delivery depends on.

A single point of failure. A freezer left unplugged after cleaning destroyed the only batch of a patient’s cells; the patient died of disease progression before a replacement could be made. The industry trades cautionary tales the way pilots trade near-misses — a dewar that tips in transit, a monitoring logger whose battery dies before the shipper does. Each is a single point of failure in a chain that offers no second copy of the product.

Overlaying all of this is the wall that most defines access: hospital readiness. Delivering a cryogenic therapy is useless unless the receiving hospital can take custody of it correctly. The last mile is the most fragile leg of all — transferring the frozen product from shipper to hospital storage, thawing it under controlled conditions, and infusing it, all without a transient warming event that could compromise potency. This requires qualified cryogenic storage on site, trained pharmacy and nursing staff, validated thawing protocols, and the machinery to manage cytokine release syndrome and other acute toxicities.

In APAC, that capability is concentrated in a small number of academic and tertiary centres in major cities. The Tier-2 hospital — the regional referral centre serving a province of several million people — is frequently unqualified to receive an advanced therapy at all. The cold chain can reach the airport. It often cannot reach the ward. And overlaying everything is regulatory fragmentation: unlike the harmonised frameworks of the FDA or EMA, APAC is a patchwork of jurisdiction-specific authorities with divergent standards — from Japan’s conditional pathways to Singapore’s risk-based model. As industry analyses have repeatedly noted, this lack of harmonisation makes cross-border trials and decentralised manufacturing materially harder, because every lane must be validated against a different rulebook.

The APAC cold-chain readiness map

The region is not one market for advanced therapies but three — sorted less by wealth than by whether the full stack (reimbursement, treatment-centre density, cryogenic infrastructure and regulatory clarity) actually connects end to end.

|

Tier & markets |

Reimbursement |

Treatment centres |

Cryo infrastructure |

Vein-to-vein feasibility |

|

Tier 1 — Established |

Reimbursed / subsidised |

Established, growing networks |

Domestic depots + LN₂ charging |

Routine and clinically viable |

|

Tier 2 — Advancing / special case |

Largely out-of-pocket / private |

Metro-concentrated, uneven |

Emerging; local manufacturing |

Viable in metros; POC bypass |

|

Tier 3 — Initialising / frontier |

None via public systems |

Few or none qualified |

Limited; dry-ice import limits |

Cross-border referral only |

Groupings synthesised from published APAC reimbursement reviews and market-readiness analyses; directional. Funding tracks the high-income tier almost exactly — and where there is no reimbursement, there is rarely the centre density or cryo infrastructure either, because none of it gets built for a market that cannot pay. The gap compounds itself.

The solutions: better boxes, better data, and moving the factory

The logistics industry has not been standing still. The response has come along three fronts.

1. The cryo-shipping stack (hardware)

Dry-vapour nitrogen shippers hold sub-−150°C conditions for validated windows of ten days or more, and are flight-compliant. Around them: ultra-low freezers, controlled-rate thaw equipment, and defence-in-depth monitoring — primary and secondary sensors, loggers engineered to outlast hold time, and geofenced alerts that fire on entry to a customs hold.

2. Digital chain-of-custody (data)

Real-time IoT telemetry — streaming temperature, location and shock — is paired with platforms that bind each shipment to an auditable chain-of-identity record. Traceability is now sold as a product: proof that a named patient’s cells stayed in specification from apheresis to infusion, giving clinicians the confidence to infuse.

3. Regional hubs and depots (network)

Cryogenic depots and treatment hubs shorten lanes rather than merely surviving them. One Cencora-owned specialist delivers more than 12,000 cryogenic shipments a year across 120-plus offices and has extended an integrated storage-and-transport cryogenic network across the region, qualified to a single global standard. A rival’s Tokyo logistics centre offers 24-hour turnaround, integrated last-mile shuttle, and co-location with a DHL-affiliated facility to reach across Korea, China and Southeast Asia. The logic is consistent: put the cold close to the patient.

The counter-model: move the factory to the patient

If the cells cannot reliably travel, the alternative is to move the factory. Point-of-care manufacturing collapses the two long cold-chain legs into a short internal walk, delivering fresh cells with vein-to-vein times of roughly 7–14 days. India’s NexCAR19 — developed out of IIT Bombay and Tata Memorial Centre, launched in 2024 — is priced near a tenth of Western equivalents (around US$50,000 against roughly US$400,000). In one point-of-care trial, therapies made on a benchtop system inside the hospital were infused fresh, with no intercontinental cold chain at all. For much of APAC, the answer to a chain that cannot span the region may be to stop asking it to.

The access implication: who the chain actually reaches

Put the pieces together and a hard conclusion emerges. The science of CAR-T is approved and, for eligible patients, frequently transformative. But the delivery system reaches a narrow slice of the region’s population — and it maps almost perfectly onto wealth, urban concentration, and infrastructure that was already there.

A patient in Tokyo, Seoul, Sydney, Singapore or Taipei sits inside a functioning system: an approved and reimbursed product, a qualified centre within reach, a validated cold chain with local depot support, and a hospital that knows how to receive and infuse. For that patient, vein-to-vein time is a clinical optimisation problem. For a patient in a Tier-2 city in Thailand or Malaysia, or almost anywhere in Indonesia, Vietnam or the Philippines, the same diagnosis leads somewhere very different. There may be no reimbursement, no qualified centre within the country, and no cold-chain lane built to serve a market that cannot pay for it. The therapy exists. It is simply not reachable.

“Approval is the beginning of a logistics question, not the end of a clinical one. In most of APAC, the honest answer to “can this patient get CAR-T” is a map question, not a medical one.”

— Health-access analyst (APAC)

The pharmacist’s view from inside a qualified hospital sharpens the point. By the time a shipper reaches the pharmacy, an enormous amount has already had to go right — thaw it correctly, get it to the bedside without a warming excursion, confirm it is the right product for the right patient. But a treating pharmacist only ever sees the shipments that made it, not the patients who were never referred because there was no route to the ward at all.

What this suggests is a region splitting into two delivery models rather than one. The first is the imported, cryopreserved, centrally manufactured therapy — extraordinary, expensive, and viable mainly for the affluent metros of Tier-1 markets and the private-pay corridors of Tier-2. The second is the locally made, point-of-care therapy — cheaper, fresher, and far less dependent on the region’s fragile long-haul cold chain — which may be the only realistic path to reaching the patients the first model structurally excludes. India has shown the second is not a compromise but, in the right hands, a clinically credible and radically more accessible route. The open question is how many other APAC markets can build the local manufacturing and hospital capability to follow.

“The dewar is a solved problem. What we are really engineering against is the gap between shipments and hospitals — the customs desk, the tarmac, the receiving dock that has never handled cryogenic material before.”

— Cryo-logistics provider (APAC lanes)

The takeaway

For years, the story of advanced therapies was a story about science: could we engineer a patient’s own cells to cure a cancer that had exhausted every other option? That question has largely been answered.

The story that will determine access across the Asia-Pacific is a different one, and it is not being told in laboratories. It is being told on loading aprons, at customs desks, in hospital receiving docks, and in the quiet arithmetic of a nitrogen dewar’s hold time against the distance to the ward. The cold chain, not the cure, is now the constraint — and the region’s choice is whether to keep extending an ever-more-sophisticated cryogenic network outward from a handful of cities, or to move the factory to the patient and shorten the chain to almost nothing. The limit on who receives an advanced therapy is no longer primarily a question of what medicine can do. It is a question of what logistics can carry — and to whom.

arcilla.fran@biopharmaapac.com

Disclaimer

This feature is published by BioPharma APAC for editorial and informational purposes only and does not constitute medical, clinical, regulatory or investment advice. Figures cited are drawn from published third-party sources, are indicative, and should be independently verified against primary sources before any reliance. BioPharma APAC is editorially independent; views expressed are those of the publication and do not represent those of any organisation named herein.

Most Read

- Can APAC Biomanufacturing Decarbonise Without Pricing Itself Out?

- The Algorithm on the GMP Floor: AI Promises a Smarter Plant. Regulators Demand the Audit Trail.

- APAC's Peptide-Capacity Gamble

- After the Rush: APAC's mRNA and Vaccine Capacity Hangover

- The Biosimilar Race: Factory to the World — or Stuck in the Copycat Economy?

- The Vein-to-Vein Problem: Can APAC's Cold Chain Carry Advanced Therapies?

- Vectors, Plasmids and the CGT Trap: APAC's Cell and Gene Therapy Ambitions Face an Upstream Bottleneck

- Can APAC Build Radioligand Therapy Before the Atoms Decay?

- The Great Biopharma Reset: 50 Developments That Changed Everything in H1 2026

- Beyond the Trial: Can Real-World Evidence Earn Regulatory Trust in APAC?

- Beyond the Obvious Giant: Where APAC's Clinical Trials Go Next

- The Frontier That Won’t Quite Arrive

Bio Jobs

- Sanofi Turns The Page As Belén Garijo Steps In And Paul Hudson Steps Out

- Global Survey Reveals Nearly 40% of Employees Facing Fertility Challenges Consider Leaving Their Jobs

- BioMed X and AbbVie Begin Global Search for Bold Neuroscience Talent To Decode the Biology of Anhedonia

- Thermo Fisher Expands Bengaluru R&D Centre to Advance Antibody Innovation and Strengthen India’s Life Sciences Ecosystem

- Accord Plasma (Intas Group) Acquires Prothya Biosolutions to Expand Global Plasma Capabilities

- ACG Announces $200 Million Investment to Establish First U.S. Capsule Manufacturing Facility in Atlanta

- AstraZeneca Invests $4.5 Billion to Build Advanced Manufacturing Facility in Virginia, Expanding U.S. Medicine Production

News