Can APAC Biomanufacturing Decarbonise Without Pricing Itself Out?

13 July 2026 | Monday | Analysis

Scope 3 clauses, single-use plastic, water and energy intensity: the “green premium” has become the defining question for the CDMOs that built Asia’s manufacturing franchise on price. Is it an unaffordable overhead — or the next axis on which the work is won and lost?

A biologics tender that crossed a Singapore business-development desk this spring arrived with an unfamiliar centre of gravity. The technical package — titres, timelines, comparability data, regulatory track record — was much as it would have been five years ago. What had changed was the annex. Running to nearly the length of the quality section sat a sustainability schedule: renewable-electricity percentage by site, a product carbon footprint expressed per gram of protein, single-use waste tonnage and its end-of-life route, water withdrawal per batch, and a line that read less like a question than an instruction — third-party-assured figures, mapped against the sponsor’s own Scope 3 reduction plan. Price still mattered. But price was no longer allowed to travel alone.

That annex is, in miniature, the story of Asia-Pacific biomanufacturing in 2026. The region assembled its extraordinary share of global drug-substance and drug-product capacity on a compound advantage: speed to clinic, engineering depth, the willingness to build ahead of demand, and — unmistakably — cost. For two decades, the pitch to a Western sponsor could be reduced to a sentence: comparable quality, faster slots, a materially lower unit price. Now a second scorecard has been laid over the first, and it does not grade on price at all. It grades on carbon, on waste, on water, and on the ability to prove all three to an auditor.

The uncomfortable arithmetic is that the two scorecards pull in opposite directions. Renewable power, water-reuse retrofits, greener solvents, waste-diversion logistics, assurance costs and the headcount to report it all cost money — and money is precisely the axis on which APAC won the work. The question the region’s manufacturers are now being forced to answer is whether sustainability has hardened into a genuine market-access requirement, and if it has, how they meet it without surrendering the price advantage that put them on the shortlist in the first place.

The pressure — the annex that won’t shrink

For most of the past decade, the pressure to decarbonise pharmaceutical supply chains came dressed as aspiration: voluntary pledges, glossy reports, a science-based target announced to applause. What changed is that the aspiration acquired teeth in the form of the buyer’s contract. Large drug sponsors, under their own reporting obligations and their own investor scrutiny, began translating sustainability from a values statement into a procurement clause. A contract manufacturer’s emissions are, by definition, part of the sponsor’s Scope 3 — the indirect, value-chain emissions that dominate a pharma company’s footprint and are the hardest to move. If the sponsor has committed to cutting Scope 3, it has, in effect, committed to cutting yours. The clause in the annex is how that commitment reaches down the chain.

The regulator eased off. The customer did not. Enforcement simply moved from the statute book to the vendor scorecard.

Underneath the reporting pressure sits a stubbornly physical one. The single-use systems that reshaped biomanufacturing — the pre-sterilised bags, tubing sets, filters and connectors that replaced fixed stainless-steel tanks — are one of the industry’s great efficiency stories and one of its most awkward waste problems at once. They eliminated cleaning validation, cut water and energy consumption, lowered capital cost and reduced cross-contamination risk. They also leave, after every campaign, kilograms of plastic that has been in contact with biological material and must be biologically inactivated before it can leave the containment suite — a step that closes off almost every conventional recycling route and sends the bulk to incineration or landfill. Add the water intensity of large-scale cell culture and downstream purification, and the energy load of running clean rooms and utilities around the clock, and the buyer’s annex is asking about real, measurable, hard-to-hide quantities.

|

The procurement view · a sourcing lead writing ESG clauses at a European biopharma “Five years ago sustainability was a tie-breaker — if two CDMOs were level on price and quality, it might nudge the decision. Now it’s a gate. If a supplier can’t give me assured emissions and a waste-handling story I can put in front of my own auditors, they don’t clear the first screen, however good the number is.” The point such buyers make is not that they will pay more for green — most insist they will not. It is that they will no longer buy dirty at any price, because the sponsor’s own reporting cannot absorb it. Cost competitiveness is being treated as necessary but no longer sufficient. |

The cost tension — when the premium is literal

The fear inside APAC’s manufacturing base is easy to state: that decarbonisation is a tax on the very thing that made the region competitive. In some line items, that fear is well founded, and the clearest example is not a metaphor but a tariff. In South Korea — home to some of the region’s largest biologics capacity — “Green Premium” is the actual name of the green-electricity option offered by the state utility, a surcharge paid on top of the standard rate for the right to claim renewable supply. Korea has long been one of the harder places in Asia to source clean power at scale; corporate renewable power-purchase agreements there have historically carried network and sleeving charges that pushed their all-in cost above conventional grid electricity. A Korean CDMO decarbonising its electricity has, quite literally, been paying a premium to do so.

Stack the rest of the ledger on top and the anxiety compounds. Water-reuse systems are capital projects with long paybacks. Greener solvents and reagents can cost more per litre than the incumbents they replace, and switching them in a validated process invites regulatory change control. Diverting single-use waste to specialist decontamination-and-recovery routes costs more than sending it to incineration. Assurance — the independent audit that turns a self-reported number into one a buyer’s auditor will accept — is a recurring fee, not a one-off. And someone has to be hired to gather, model and file all of it. For a business whose entire value proposition is a lower unit cost, every one of these is a headwind against the franchise.

Yet the ledger is not one-directional, and the manufacturers pulling ahead have grasped that the framing of “green versus cheap” is partly false. A large share of the credible decarbonisation moves are cost-neutral or actively cost-saving. Single-use technology itself, whatever its waste footprint, cuts water and energy use dramatically against stainless steel. Energy-efficiency and lean-manufacturing programmes reduce carbon and cost in the same motion — one leading regional player has catalogued hundreds of discrete energy-saving cases across its network, the overwhelming majority of them delivering both an environmental and an operational return. And the electricity picture is shifting: in Korea, renewable PPAs that once sat well above grid prices have, by 2025, closed in on parity for many load profiles as conventional tariffs rise. The premium, in other words, is real in places, vanishing in others, and occasionally negative. The skill is knowing which is which — and sequencing accordingly.

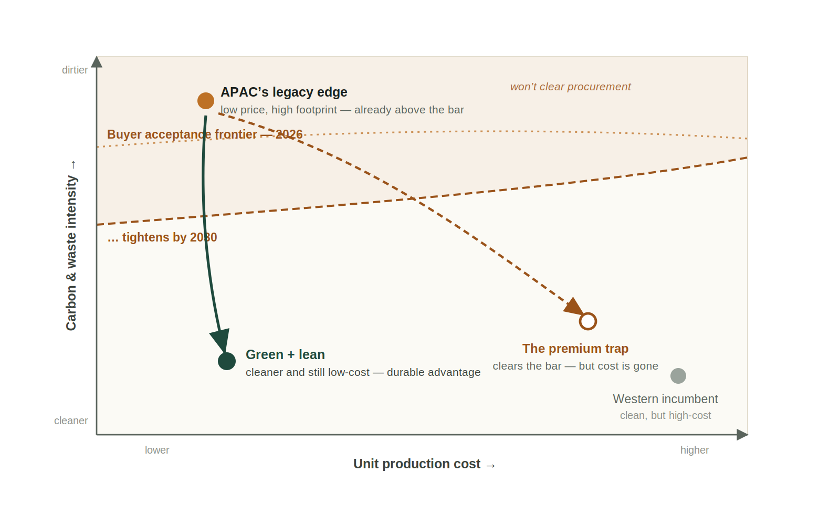

FIGURE 1 · THE EMISSIONS–COST TRADE-OFF, MAPPED

Standing still already fails the buyer. The question is which way you move.

How to read it. The vertical axis is carbon-and-waste intensity; the horizontal axis is unit cost. The dashed lines are the moving threshold below which a supplier’s footprint has to fall to clear a buyer’s procurement screen — a line that keeps descending. APAC’s historic position (low cost, high intensity) now sits above the frontier: standing still is not an option. Adding green capex without touching efficiency drags a firm down and right — compliant but priced out. Folding decarbonisation into yield, energy and waste discipline drops intensity while holding cost. Conceptual schematic; axes are illustrative, not to scale.

|

The EHS / sustainability lead · an environment & energy head at an APAC CDMO “The board hears ‘sustainability’ and thinks cost centre. My job is to show them that most of my roadmap is the efficiency roadmap wearing a different badge — the kilowatt-hour I don’t burn and the batch of media I don’t waste are carbon and margin. The genuinely expensive items are a short list, and I sequence those for when a client will pay for them or when a PPA has hit parity.” |

BY THE NUMBERS — THE SHAPE OF THE SHIFT

|

39.8% Samsung Biologics’ renewable-electricity transition rate under its RE100 roadmap, up year on year (2026 ESG report) |

~80% Estimated share of companies removed from the CSRD’s mandatory scope by the EU’s 2026 Omnibus threshold change |

~70% Water saved by single-use technology versus stainless-steel processing, per WuXi Biologics’ green-manufacturing figures |

The solutions — making green cheaper than it looks

If the pressure is real and the cost tension is genuine, the interesting question is operational: how are the region’s most advanced manufacturers actually closing the gap? The answers cluster into four moves, and the common thread across the credible ones is that they treat decarbonisation as process engineering rather than as a bolt-on compliance expense.

Renewable power, bought carefully

The largest players are converting their electricity supply on published roadmaps rather than gestures. Samsung Biologics, which joined the RE100 initiative in late 2022 with a commitment to fully renewable electricity by 2050, reported its transition rate rising to 39.8 per cent in its 2026 ESG disclosures, alongside an expansion of Scope 3 emissions-reporting coverage from 56.3 to 63.7 per cent of its value chain and an ‘A’ rating for water security from the environmental disclosure body CDP. Crucially, it has had its product-carbon-footprint methodology independently validated — the difference between a number a client hopes is right and one their auditor will accept. Across the industry, procurement teams are learning to distinguish between renewable-energy certificates, which are cheap but weak on additionality, and power-purchase agreements, which cost more upfront but carry real environmental weight and reputational durability. The sophistication is no longer whether to buy green power, but which instrument buys the most credible tonne per dollar.

Single-use waste: from disposal to recovery

The plastic problem is the hardest of the four, precisely because contamination-control rules block the easy answer. Material that has touched product must be inactivated before it can leave containment, which rules out ordinary recycling. Two responses are maturing. The first is materials innovation — single-use components built from mechanically recyclable polymers or bio-based feedstocks — though these face a regulated-industry friction all their own, since changing the material in contact with a drug can trigger a post-approval change filing. The second is decontamination-then-recovery: validated on-site treatment that renders waste safe so it can be mechanically recycled or sent to waste-to-energy rather than landfill. One such program in the United States has helped a cluster of manufacturers recycle more than 2,800 tonnes of single-use waste; the model is not trivial to replicate everywhere, but it establishes the principle. Leading regional CDMOs now pair aggressive source-reduction with zero-waste-to-landfill and waste-to-energy commitments, and continue to hunt for regulator-acceptable recycling routes. And a point that gets lost in the plastic anxiety deserves restating: life-cycle assessments consistently find that single-use, for all its solid waste, reduces overall energy demand and warming potential against stainless steel — the waste is visible, the savings are not.

Water reuse and greener chemistry

Water withdrawal per batch is increasingly a line item buyers track, and closed-loop reuse of process and utility water — recovering, treating and recirculating rather than drawing fresh — is moving from pilot to standard at newer facilities. On the chemistry side, the gains come from solvent reduction and substitution, process intensification and higher yields that shrink the footprint per gram of output. The most striking claimed figures come from combining digital process design with single-use operations: WuXi Biologics has reported that pairing its process-development platform with single-use technology can cut the product carbon footprint per gram of protein by up to 80 per cent — a reduction achieved not by spending on offsets but by making the process itself leaner.

|

The single-use & waste specialist · a bioprocess sustainability consultant “People want a villain, and the plastic bag is convenient. But the honest life-cycle picture is that single-use saved enormous water and energy — the failure was never building the end-of-life infrastructure to match. The plants that will win the next decade are the ones investing in decontamination and recovery now, while it’s still a differentiator and not yet a baseline everyone is forced into.” |

The competitive reframe — growth or cost?

Strip away the branding and the logic is genuinely competitive. A contract manufacturer that can hand a buyer an independently assured, low product-carbon-footprint number is not absorbing an overhead — it is selling something the buyer urgently needs and cannot easily source elsewhere: a verifiable reduction in the buyer’s own hardest-to-move emissions. That reframes the whole economics. Samsung Biologics’ decision to offer clients product-carbon-footprint assessments is the same play from a different angle. In both cases sustainability stops being a cost the CDMO eats to stay on the list and becomes a differentiator that raises the switching cost of leaving. As its president John Rim put it in the company’s latest report, sustainability has become part of how the business creates long-term value — language that, a few years ago, would have been read as public relations and is now read by procurement as product.

A verifiable low-carbon batch is not an overhead the manufacturer eats. It is a Scope 3 reduction the buyer can’t get anywhere else — and will pay to keep.

|

The ESG analyst · a healthcare sustainability analyst “The market is bifurcating. A first tier is turning decarbonisation into a commercial capability and pricing it into stickier client relationships. Everyone else is treating it as a compliance cost they’ll pay late, under pressure, at a worse price. The gap between those two groups is going to widen, and it will show up in who holds onto the high-value Western work as the pure cost arbitrage narrows.”

|

The takeaway — tax or moat

Return, finally, to the annex on that Singapore desk. Is the schedule of carbon, waste and water figures it demands an unaffordable overhead bolted onto a shrinking price advantage — or the next basis on which APAC’s manufacturing work is won? The honest answer is that it is both, and which one it becomes for any given manufacturer is a choice being made right now, not a fate being handed down.

For the firm that treats decarbonisation as compliance — a box to tick, a report to file, a certificate to buy — it will be a tax. It will layer real cost onto a business whose entire proposition was low cost, at precisely the moment other pressures are already narrowing the arbitrage that built the franchise. For the firm that treats it as engineering — folding carbon, energy, water and waste into the same operational discipline that made it efficient in the first place, and then selling the resulting verified performance back to the buyer as a service — it becomes a moat. The efficiency and the emissions fall together; the assured number becomes a reason to stay rather than a cost to bear.

The green premium is real, and in places — a Korean utility bill, a solvent swap, an assurance fee — it is literal. But the region that learned to build biologics capacity faster and cheaper than anyone expected is not obviously the region that will find it hardest to make that capacity clean. The uncomfortable truth for the sceptics is that decarbonisation, sequenced well, looks a great deal like the cost discipline APAC already mastered. The manufacturers who see that first will not be pricing themselves out. They will be pricing the competition out of a market that has quietly changed what it is buying.

(arcilla.fran@biopharmaapac.com)

|

Disclaimer: Figures and statements attributed to named companies (Samsung Biologics, WuXi Biologics) are drawn from those companies’ own public disclosures, sustainability reports and executive remarks published in 2025–2026. Perspectives labelled “composite” are illustrative syntheses of positions commonly voiced across the industry by professionals in the relevant roles; they are not quotations from, and should not be attributed to, any specific named individual. Regulatory details — including the CSRD and the 2026 Omnibus amendments — are summarised for context and continue to evolve; readers should verify against primary sources. Nothing here constitutes investment, legal, compliance or procurement advice. |

Most Read

- How Does GLP-1 Work?

- Innovations In Magnetic Resonance Imaging Introduced By United Imaging

- Management of Relapsed/Refractory Multiple Myeloma

- 2025 Drug Approvals, Decoded: What Every Biopharma Leader Needs to Know

- BioPharma Manufacturing Resilience: Lessons From Capacity Expansion and Supply Chain Resets from 2025

- APAC Biopharma Review 2025: Innovation, Investment, and Influence on the Global Stage

- Top 25 Biotech Innovations Redefining Health And Planet In 2025

- The New AI Gold Rush: Western Pharma’s Billion-Dollar Bet on Chinese Biotech

- Single-Use Systems Are Rewiring Biopharma Manufacturing

- The State of Biotech and Life Science Jobs in Asia Pacific – 2025

- Asia-Pacific Leads the Charge: Latest Global BioSupplier Technologies of 2025

- Invisible Threats, Visible Risks: How the Nitrosamine Crisis Reshaped Asia’s Pharmaceutical Quality Landscape

Bio Jobs

- Sanofi Turns The Page As Belén Garijo Steps In And Paul Hudson Steps Out

- Global Survey Reveals Nearly 40% of Employees Facing Fertility Challenges Consider Leaving Their Jobs

- BioMed X and AbbVie Begin Global Search for Bold Neuroscience Talent To Decode the Biology of Anhedonia

- Thermo Fisher Expands Bengaluru R&D Centre to Advance Antibody Innovation and Strengthen India’s Life Sciences Ecosystem

- Accord Plasma (Intas Group) Acquires Prothya Biosolutions to Expand Global Plasma Capabilities

- ACG Announces $200 Million Investment to Establish First U.S. Capsule Manufacturing Facility in Atlanta

- AstraZeneca Invests $4.5 Billion to Build Advanced Manufacturing Facility in Virginia, Expanding U.S. Medicine Production

News

Editor Picks